Shell Names the Risks and Discounts Them to Zero

Shell describes the world we live in, models a different one, and doesn’t seem to notice the mismatch.

Its 2026 Energy Security Scenarios lays out the constraints of our planetary predicament with unusual clarity. It starts from a premise I agree with: the world is changing fast enough that business-as-usual modeling is no longer useful. Geopolitical and social tensions, a fragmenting world order, and growing uncertainty about growth, trade, and supply chains complicate energy supply and demand. Add AI-driven electricity demand, climate disruption, and the legitimate aspirations of billions in the developing world, and complexity only intensifies.

Then the report pivots. From that realistic starting point, Shell’s modeled outcomes read like technological wish-fulfillment: sustained global GDP growth above 3% per year, electricity becoming the dominant form of energy by mid-century, EVs as the default car, and commercial nuclear fusion in barely more than a decade.

Three long-term scenarios are offered with Shell’s usual cute names, but I’m only going to discuss what I consider the closest thing to a base case. Archipelagos is described as a fragmented world where nations prioritize self-interest and security. This drives regional conflict, competing trade blocs, and a renewed emphasis on domestic energy supply. Renewables expand, but fossil fuels remain dominant because weak growth and limited coordination slow grid modernization. Intermittency remains a stubborn constraint: storage, transmission, and interconnection scale too slowly to fully integrate wind and solar. Climate policy is similarly constrained by trade barriers and geopolitics, so the world passes 1.5°C and drifts toward 2.5°C by 2100, with adaptation taking precedence over mitigation. AI matters but fails to meet its promise because the grid can’t add electric power fast enough.

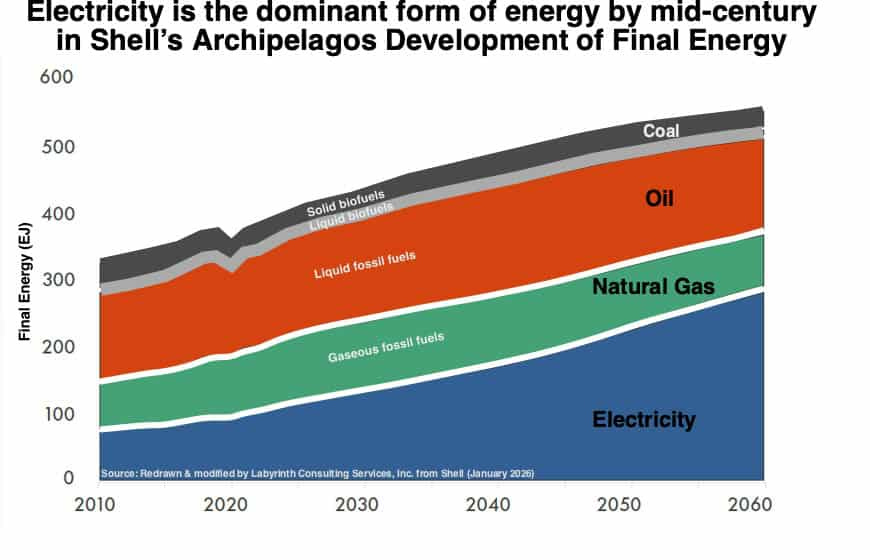

That framing is close to my own, which is why the projections surprised me. Figure 1 shows a shift toward full electrification by 2060 while fossil fuels shrink only modestly. The narrative stresses fragmentation, slower coordination, and constrained optimization. But the projections don’t reflect oil and gas depletion or any change in affordability. What stands out is a system-wide buildout of the one thing that requires the most coordination: electrified infrastructure at scale.

Shell’s modelers are not neutral observers, especially when the document states that “electrification is critical to achieving net zero emissions.” That may be true, but a scenario model shouldn’t be endpoint-loaded. It should move forward from history, starting conditions, and constraints. If the results align with expectations, fine. But it’s not credible to force the conclusion into the model and then present the output as if it emerged from the world being described.

Shell explicitly acknowledges that “much greater use of electricity will involve a substantial increase in demand for certain minerals.” That’s not a minor detail. Copper is the choke point because electrification is fundamentally more wire, more motors, more transformers, more generators, and more transmission. Then come the battery materials: lithium, graphite, nickel, cobalt, and manganese, along with large volumes of aluminum, steel, and high-purity silicon.

Wind and solar add their own constraints. Wind requires rare earths in some turbine designs, specialty steels, and massive concrete foundations, often far from power load centers. Solar needs large volumes of copper and aluminum, plus even tighter inputs like silver and polysilicon. None of these supply chains should scale smoothly. Mines and processing take years to build, ore grades decline, refining is energy- and water-intensive, and key steps are concentrated in a handful of countries now drifting into a kind of cold war with one another. In practice that means uneven growth, price spikes, delays, forced substitutions, and periodic shortfalls that show up precisely when you try to accelerate deployment.

But Shell’s output in Figure 1 shows a smooth climb from roughly one-fifth to more than half of global electricity consumption in a single generation. How is that possible in the world that Shell describes?

Shell doesn’t seem to consider path dependence at all. Renewable equipment has a working life of about 25 years. The buildout isn’t a one-time event; it’s a treadmill. If you install first-generation infrastructure in the 2025–2040 window, you’re going to replace a lot of it in the 2050–2065 window at the same time you’re still trying to expand the system. The replacement wave competes for the same copper, lithium, graphite, manufacturing capacity, and skilled labor as the first expansion wave. It’s unclear whether there will be enough materials for the second generation at comparable cost and scale, but if it exists, bottlenecks, overruns and backlash from the first wave will cascade into the second.

When Shell acknowledges mineral demand pressures but still projects electricity rising to more than half of final energy by 2060, there’s a major mismatch.

In Archipelagos, Shell’s model has wind and solar supplying more than 60% of global electricity by mid-century (Figure 2). That’s a breath-taking leap from roughly 6% today that demands more than “and then a technological miracle happens.” It requires an economic justification for how a fragmented, fiscally fragile world finances and executes the most coordination-intensive buildout in modern history.

.")

There is a widespread belief that wind and solar are the cheapest energy sources ever built. But that rests on a narrow, project-level measure like Lazard’s Levelized Cost of Energy (LCOE). LCOE asks a limited question: what does it cost to generate one megawatt-hour at the project fence line? It largely ignores what matters to the grid: the cost of turning intermittent, weather-driven output into reliable power on demand. It’s like buying a house and thinking the sale price is the end of living expense—no insurance, taxes, maintenance and repairs, or monthly gas and electricity bills.

Renewable economics change once wind and solar are asked to behave like real power plants. I asked a different question than LCOE asks: what does it cost to add 1 GW of wind or solar that functions like a responsible, dispatchable generator in practice, firmed with backup, integrated into the grid, and financed at a 6% real cost of capital?

In a MISO-type region, once wind and solar are required to carry full system responsibilities, the economics unravel. At a real world wholesale power price of $50/MWh (5¢/kWh) to producers, neither solar nor wind breaks even in discounted terms (Figure 3). Even under optimistic assumptions, solar never gets there, and wind only reaches breakeven after roughly 35 years. That is a real problem in the kind of fragmented, capital-constrained world Shell describes in Archipelagos.

To Shell’s credit, it describes grid integration as a real constraint. The report devotes an entire section to the challenges of integrating intermittent renewables, explicitly acknowledging that high renewable penetration requires additional infrastructure, balancing capacity, and system-level investment beyond the generation project itself. What doesn’t happen is a hard accounting of total system cost—the kind shown in my Figure 3. In Archipelagos, electricity expands as if firming, backup, transmission, and storage are frictionless add-ons rather than the cost drivers that determine whether the buildout makes sense to investors and lenders.